In October, the IRS announced 2026 penalties for failure to file or furnish ACA reporting forms and published an FAQ clarifying certain infertility benefits and the 2026 Cost of Living Adjustments. California expanded its Paid Family Leave program to include “designated persons” and enacted a groundbreaking bill impacting pharmacy benefit managers.

2026 Penalties for Failure to File or Furnish ACA Reporting

Forms 1095-C and 1094-C

The IRS has announced the 2026 penalties for failure by Applicable Large Employers (ALEs) to file or furnish Affordable Care Act (ACA) reporting Forms 1095-C and 1094-C for the 2025 tax year. Amounts can increase significantly depending on how late the filing is or if the failure is determined to be intentional disregard.

Filing is due by March 31, 2026, if filing electronically, or by Feb. 25, 2026, if filed on paper.

Penalty structure:

- Incorrect or late reporting: $340 per form

- Failure to file with the IRS and failure to furnish a statement to an employee: $340 per form

- If the IRS finds that the failure to file or furnish was due to intentional disregard: $680 per return, with no annual maximum.

- If the failure is corrected within 30 days of the due date, the penalty is reduced to $60 per return.

- If the failure is corrected more than 30 days after the deadline but by Aug. 1, 2026, the penalty is $130 per return.

IRS Releases FAQ on Affordable Care Act Implementation

On Oct. 16, 2025, the Departments of Labor, Health and Human Services, and Treasury (the “Agencies”) released FAQ 72: Affordable Care Act Implementation, clarifying that certain fertility benefits may qualify as “excepted benefits” under federal law. The guidance, issued with a White House Fact Sheet and in connection with the 2025 Executive Order on Expanding Access to In Vitro Fertilization(IVF), outlines new opportunities for employers to offer fertility coverage outside of traditional group health plans.

Expanding Access Through Excepted Benefits

Employer-sponsored health plans are subject to extensive federal requirements under the Affordable Care Act (ACA), Health Insurance Portability and Accountability Act (HIPAA), and the Employee Retirement Income Security Act (ERISA). “Excepted benefits” are exempt from many of these provisions.

Under the new guidance, fertility benefits may now qualify as excepted benefits, making them easier for employers to offer. The coverage could be offered through a standalone plan, similar to dental or vision benefits, rather than embedding such benefits within a major medical plan.

Independent, Non-Coordinated Excepted Benefits

One option for employers is to offer fertility coverage as an independent, non-coordinated excepted benefit. To qualify, the benefit must be:

- Provided under a separate policy, certificate, or contract of insurance;

- Independent from any exclusions under the employer’s primary health plan; and

- Payable without regard to whether benefits are available under another group plan from the same sponsor.

Importantly, this benefit must be fully insured. Employees can enroll in a standalone fertility policy without enrolling in the employer’s group health plan, and participation will not disqualify them from contributing to a health savings account (HSA) if they are covered by a high-deductible health plan.

Limited Excepted Benefits

The FAQs also clarify that fertility coverage can be structured as a limited excepted benefit, the same category that applies to dental, vision, and employee assistance plans (EAPs).

Employers may offer an excepted benefit health reimbursement arrangement (HRA) to reimburse fertility-related out-of-pocket expenses, subject to specific conditions:

- The HRA must be entirely employer-funded, with no employee premiums or cost-sharing.

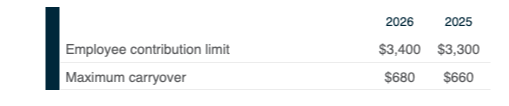

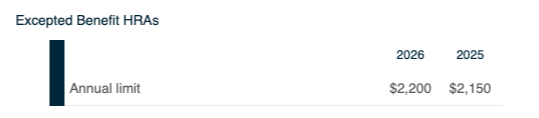

- A benefit cap of $2,150 must apply for plan years beginning in 2025 and $2,200 for 2026.

- Coverage must remain separate from the main group health plan.

Employers may also provide fertility coaching or navigation services through an EAP that qualifies as a limited excepted benefit, as long as the EAP does not offer significant medical treatment. Fertility treatment itself must be provided under a separate group health plan to preserve the EAP’s excepted benefit status.

Employer Considerations

The Agencies plan to issue proposed regulations expanding the ways fertility benefits can qualify as limited or supplemental excepted benefits. They are also considering updates to current limits (such as the 15% cap on the cost of supplemental coverage relative to primary health coverage) to allow more flexibility for employers.

IRS Releases 2026 COLAs

The IRS has issued 2026 cost-of-living adjustments for several provisions of the Internal Revenue Code that affect employer-sponsored benefit plans.

Health Flexible Spending Arrangements (FSAs)

Qualified Transportation Benefits

Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs)

Excepted Benefit HRAs

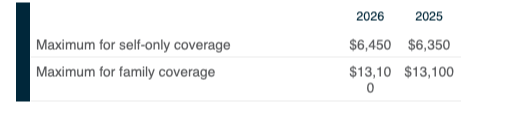

Health Savings Accounts (HSAs)

Highly Compensated and Key Employee Thresholds for Nondiscrimination Testing

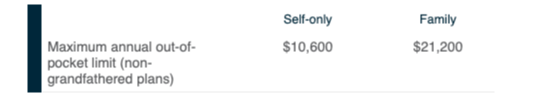

Group Health Plan Cost-Sharing Limits

Employer Considerations

Employers with plan years beginning on or after Jan. 1, 2026, should update plan documents, payroll systems, and employee communications to reflect these new limits. Reviewing nondiscrimination testing thresholds and benefit designs now will help ensure a smooth transition into the 2026 plan year.

California Expands Paid Family Leave Program

California has expanded its Paid Family Leave (PFL) program to better reflect the diverse relationships that shape modern caregiving. Governor Gavin Newsom recently signed Senate Bill (SB) 590, extending state-paid family leave benefits to employees who take time off to care for a “designated person,” defined as someone related by blood or whose relationship is equivalent to that of family.

This legislation builds on Assembly Bill (AB) 1041, passed in 2022, which first allowed employees to take job-protected leave under state law to care for a designated person.

However, at that time, the state’s PFL program did not provide wage replacement benefits for such leave. SB 590 now aligns the benefit structure with the leave entitlement, ensuring that eligible employees can receive financial support when caring for those who are like family, even if not legally or biologically related.

Beginning July 1, 2028, California workers will be able to claim PFL benefits to care for a designated person. When applying, employees must identify their designated person and attest, under penalty of perjury, how that individual qualifies, whether through blood relation or an equivalent close bond.

SB 590 marks a significant step in recognizing the importance of caregiving relationships beyond traditional definitions of family, supporting a more inclusive and compassionate approach to employee leave.

Employer Considerations

Employers can mark their calendar to prepare appropriate documents prior to the start date of July 1, 2028.

California Enacts New PBM Law

California has enacted Senate Bill 41, a groundbreaking new law that redefines how pharmacy benefit managers (PBMs) operate in the state. Signed by Governor Gavin Newsom, the law strengthens oversight, transparency, and fairness in the prescription drug marketplace—changes that will have meaningful implications for employers, health plans, and pharmacies.

SB-41 gives employers and plan sponsors greater control and clarity over pharmacy benefit costs, ensuring that rebate savings flow directly to their plans and participants. By mandating fiduciary responsibility and transparency, California’s new PBM framework empowers HR and benefits leaders to negotiate more effectively and align pharmacy benefits with organizational goals for affordability and fairness.

Key Points for Employers and Health Plans

- Fiduciary duty and licensing.

PBMs must now act in the best interests of their clients, including employers and health plans, and maintain state licensing through the Department of Managed Health Care (DMHC), which will conduct routine audits. - Full rebate pass-through and ban on spread pricing.

PBMs must pass 100% of manufacturer rebates directly to the payer and accept as compensation only fees that are not tied to drug price metrics. They are prohibited from profiting through spread pricing. - Transparency and reporting.

PBMs are required to share detailed quarterly reports on pricing, rebates, and pharmacy arrangements upon request, providing better visibility into how dollars are spent. - Fair pharmacy practices.

The law prohibits steering patients to PBM-affiliated pharmacies, requires equal reimbursement terms, and eliminates extra transmission fees on pharmacy claims. - Patient protections.

Health plans cannot charge members more than the actual cost of their prescriptions, and PBMs may only enter exclusive drug contracts that result in lower costs for both plans and patients.