IRS Announces Increased Limits for Certain Employee Benefits, Higher Fines for ACA Reporting Failures

Each year, just as the leaves turn to the fiery shades of autumn, the Internal Revenue Service (IRS) announces how much more “green” will be available during the coming year under various employee benefit programs. The IRS recently released Revenue Procedure 2022-38 in which it has updated many key employee benefit limits based on annual inflation or cost-of-living adjustments. The good news is that recent higher inflation trends have led to the IRS providing for higher-than-typical increases in both the amount that individuals can contribute to a health flexible spending arrangement (HFSA), as well as the amount they can carry over in a plan including that feature.

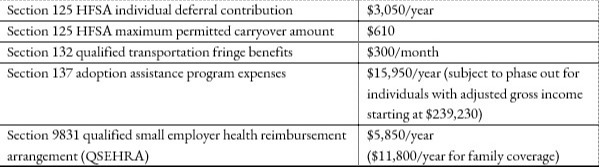

Effective for tax years beginning in 2023, the following higher limits will apply:

Employers should keep the adjusted limits handy as they prepare for 2023 and communicate with their employees regarding various benefit options.

Additionally, the IRS has announced that employers that fail to file ACA Forms 1095 in 2024 (reporting for 2023) can be subject to a $310 penalty per form. The updated penalty for failure to provide individual statements to employees also will increase to $310 per statement. Since the penalties are cumulative, an employer that fails to provide an employee statement and fails to file with the IRS can be penalized up to $620 for each required form.

As we have noted previously, the IRS continues to be less lenient with late ACA report filers. As fines continue to increase, employers with filing obligations should take great care to ensure that their reporting processes ensure timely filing and timely distribution of individual statements.